Independent Valuation & Pricing policy under AIFMD

Under the Alternative Investment Fund Management Directive (AIFMD) – which came into force in July 2011, Alternative Investment Fund Managers (AIFM's) are required to establish, maintain, implement and review for each Alternative Investment Fund (AIF), appropriate and consistent written policies and procedures for the valuation of assets across the fund.

Peter Jones

Senior Partner - Voltaire Advisors

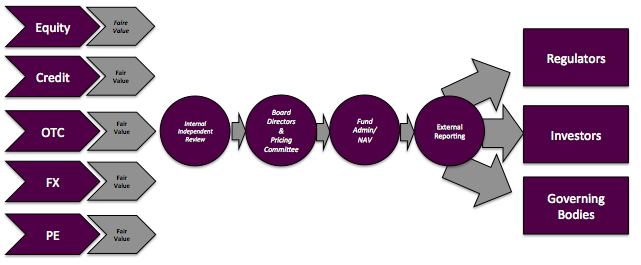

The Valuation Governance Chain

Areas of focus for the AIFM & Independent Valuation Function:

AIFM’s need to establish the governance of the valuations under the AIFMD regulatory framework and need to maintain, implement and review for each AIF the written controls, policies and procedures for the valuation of assets within the AIF. The objective is to produce unbiased, transparent and sound valuations with due care and skill. Valuations will need to adhere to IFRS accounting levels and national and international valuation standards and guidelines.

Policies must outline valuation methodology for each asset class and be applied consistently across all assets within the AIF. It is best practice for the AIFM to apply consistent and systemic processes across all the funds it manages. The AIFM’s must also establish processes for governing the appropriate use of models, sourcing of market data, documentation of assumptions and rationale for use of models.

Where the AIFM performs the Independent Valuer function the policy must include:

- Detail of how any conflict of interest is mitigated.

- How the AIF asset valuation policies will be reviewed to ascertain compliance.

Policies must be reviewed annually.

AIFM’s will focus on the risk of bias within the AIF investments – specifically.

- Unquoted & illiquid asset valuation.

- Complex & hard to value assets – where subjectivity/judgement is used/needed.

AIFM’s must show that valuation process and governance is in place to mitigate conflicts of interest. AIFM’s should demonstrate:

- Competence and independence of personnel carrying out valuations.

- Investment strategies of the AIF & assets the AIF may invest in.

- Controls over the selection of valuation inputs, sources and methodologies.

- Process & channels for valuation “exception” escalation, review and resolution.

- Policies and documentation of how adjustments are made for liquidity/size or market conditions.

- Consistent book valuation and timing process.

- The frequency of valuing assets.

- The review process for assets where material risk exists (material risks e.g. subjective judgement /internal models used).

- Review process where valuation is based on single counterparty or broker source.

Models used by AIF must be approved by the AIFM:

- Documentation of models must outline decisions for choosing underlying data sources and assumptions used, rationale and limitations.

- Models must also be validated by appropriate person not involved in using the model.

In short, the level of governance, oversight, documentation and transparency relating to asset valuation under AIFMD far exceeds anything that AIFM’s have yet experienced. In all but the largest such managers this will place great strain on operational resources already dealing with the myriad other requirements of the Directive.